The supply of solar panels is not a problem, but other bottlenecks during installation have emerged, according to a report by Clean Energy Associates.

Clean Energy Associates (CEA) has released a global report on the supply of PV cells and modules, noting that the United States supply chain is “more than adequate” for current deployment levels.

The report notes that slow implementation in the second and third quarters of 2024 has led to sufficient supply from PV imports.

However, CEA highlighted two potential bottlenecks for installation in the United States: the supply of transformers and a lack of skilled labor.

CEA said U.S. utilities have restrictions on what types of transformers can be used in regional projects. These restrictions typically require non-Chinese equipment. However, the supply of transformers outside China is limited and not designed for large-scale mass production.

“Most foreign transformer companies compete with China, are conservative in expansion, and transformers are labor-intensive and highly customized per order,” the report said.

CEA noted that transformer suppliers have announced significant expansions of new production in the United States, but it will take several years for new production to come online and support demand growth.

As for labor shortages, this problem is less pronounced, CEA said. The number of workers available for each vacancy in the construction sector remains virtually the same, with 1.09 workers available for each job. CEA said that while there are currently no labor shortages, the relative parity means that there are sometimes labor market bottlenecks for engineering, procurement and construction (EPC) companies to undertake a growing number of projects.

Product types

CEA’s global supply report covers a wide range of solar production and supply-related issues.

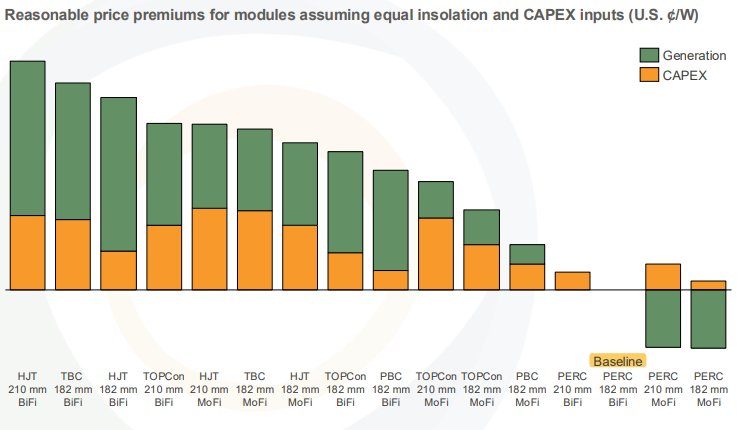

The report noted that the average winning bids for module supply deals in the Chinese market are approximately $0.10 per W. It also highlighted that almost all new public tenders are for n-type solar products, with HJT charging a higher price.

Additionally, bifacial products, or solar modules that capture and convert sunlight on both sides, have seen price increases due to their higher yield compared to monofacial modules. The chart below shows the relative capital expenditure and production output of leading module sizes, with pricing details in the full report.

This content is copyrighted and may not be reused. If you would like to collaborate with us and reuse some of our content, please contact: editors@pv-magazine.com.

Popular content